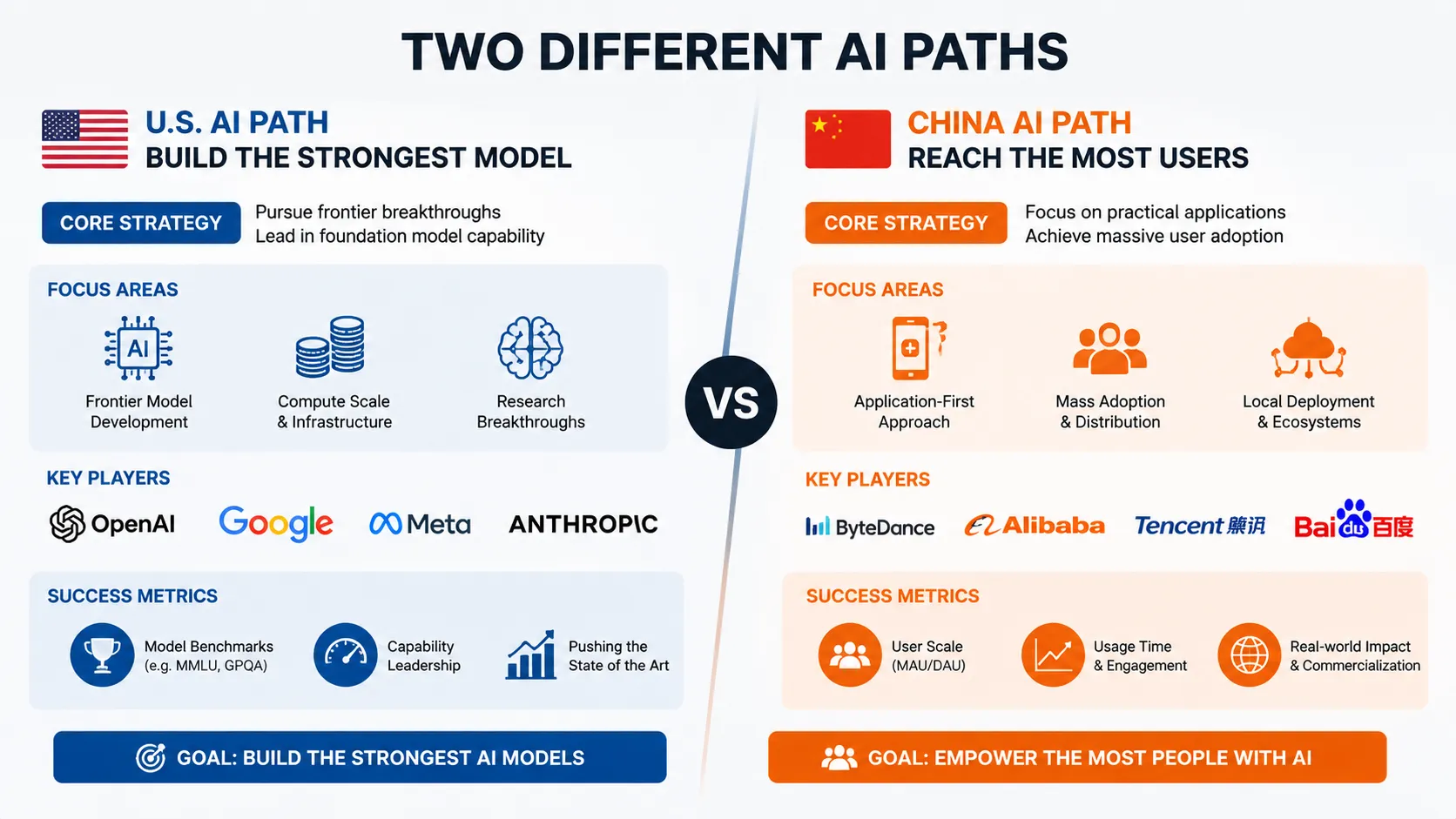

Washington Post’s latest report, filed from Singapore, frames the global AI competition in a way that cuts against the prevailing narrative in Washington. U.S. companies are trying to build the smartest model. Chinese companies are trying to build the most-used one.

Numbers back this up. Chinese AI models now account for about 40 percent of global token usage, and have led U.S. models in weekly call volume for eight consecutive weeks on OpenRouter. That‘s not a technical advantage. It’s an adoption advantage.

MiniMax‘s global business manager put it directly: the goal isn’t technical benchmarks — it‘s “how many people around the world are actually using our products every day.” That’s a different metric than the ones U.S. labs publish in their model cards.

JPMorgan‘s geopolitical center noted in a May report: “Top models may converge near the frontier, but outcomes increasingly depend on prompt quality, tools and domain integration.” In plain English: the performance gap between the best model and the second-best is getting narrower. The gap in who actually uses them is getting wider.

80% of the Value at 10% of the Cost

Affordability gap is stark. UBS estimates that Chinese model training costs are less than 10 percent of those for OpenAI and Anthropic, while average API pricing is about 20 percent lower than comparable global peers.

A Chinese AI company sales representative’s framing was even more pointed: “If we can provide 80 percent of the value at a fraction of the cost, that‘s enough. That portion of the market is ours.”

Lindy is often cited. This AI startup switched from Anthropic’s Sonnet to DeepSeek V4 and cut its costs to one-tenth of what they were, saving millions of dollars.

Zhipu‘s product director compared the two approaches directly: U.S. companies are selling Rolls-Royces. Chinese companies are selling Mercedes — slightly less premium, but more affordable and more widely available.

As UBS analysts noted, as AI moves from experimentation to scaled deployment, companies are shifting from “maximizing token usage” to “ROI-sensitive resource allocation.” That shift favors cheaper models.

Open-Source Is a Distribution Strategy

Chinese AI models are mostly open-source. That’s not a technical decision. It‘s a distribution strategy. Companies can download and deploy them locally, which appeals to businesses handling sensitive data and those worried about API price hikes or access being cut off.

A Russian entrepreneur based in Thailand told the Post that his AI banking startup is built entirely on Qwen because he wants to keep his data under local control. “Companies that use cloud systems sometimes have data leaks,” he said. “I can’t allow that. This model suits me better.”

That‘s not an argument about which model is smarter. It’s an argument about which model is safer to build a business on.

Export Controls Became Free Advertising

Timing matters. On June 12, the US government imposed export controls on Anthropic‘s Fable 5 and Mythos 5, cutting off non-US access. Same week, Zhipu’s stock surged nearly 50 percent.

Martijn Rasser, a vice president at the Special Competitive Studies Project, told the Post: “Users now have reason to worry about the reliability of American AI products. That‘s not an attractive feature.” A Chinese AI executive was blunter: “American policies are becoming free advertising for Chinese AI.”

Contrast is not subtle. US is restricting access to its models. China is making its models available to anyone who wants them. One approach builds scarcity. The other builds market share.

The Market the US Is Leaving Open

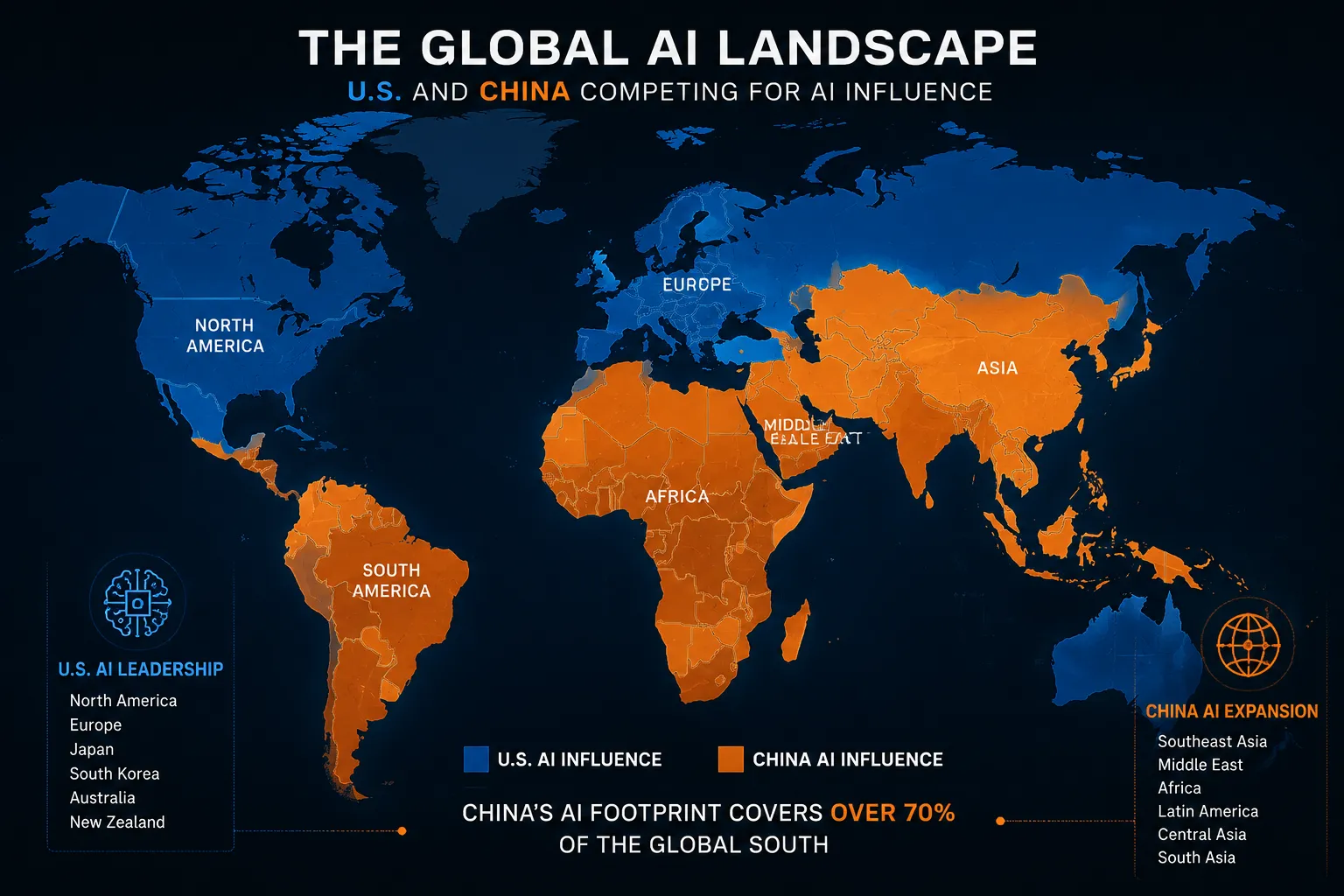

Post’s reporting maps out where Chinese AI is already embedded. Singapore government-backed AI projects are being built on Alibaba‘s Qwen. Saudi Arabia is working with ByteDance and Huawei on AI for city infrastructure. Malaysia’s $2 billion “smart city” initiative includes plans for a Chinese AI research center.

China is not trying to beat the US on AI benchmarks. It‘s trying to win the market that the US is leaving open — the global South. As the vice chairman of a Ghanaian think tank put it, “People in Africa cannot afford very expensive solutions beyond open-source options.” That’s not a hard choice. It‘s the only choice.

Frontier vs. Floor

US AI narrative is about the frontier. Chinese AI narrative is about the floor. UBS estimates the long-term AI market opportunity could exceed $10 trillion, and Chinese models have “considerable room” to increase their global share.

As one analyst put it, global model market will become “increasingly stratified.” Frontier models will still command a premium for complex tasks, but for high-volume, ROI-sensitive workloads, cheaper models will win — and that’s precisely where Chinese models are positioned. That‘s not a technical argument. It’s a market argument. And markets tend to move toward cheaper options.

P.S. US is trying to win by being the best. China is trying to win by being the cheapest and most available. Race isn‘t over — but it’s being run on two different tracks. If the cost gap persists, one track might produce a lot more finishers.