Useful AI has arrived, and it is profitable. Huang said it twice during the shareholder meeting. Not as a prediction. As a statement of fact.

He didn’t stop there. He described AI data centers as“factories that manufacture tokens.” Tokens become code, answers, designs, actions, and services. Every token is a unit of profit.

His logic is simple. If tokens are assets, the factories that produce them shouldn‘t be valued like cost centers. Nvidia’s customers aren‘t buying servers. They’re building revenue-generating AI factories. The distinction matters for how Wall Street prices the entire AI ecosystem.

He Was Answering Wall Street‘s Biggest Question

For months, analysts have been asking the same question. When does AI spending turn into AI revenue? High-profile cases like Uber burning through its annual AI budget in four months have made that question louder. Oracle’s massive quarterly capex and negative free cash flow have also fueled skepticism. Markets have been wondering if the spending binge is sustainable.

Huang answered that question directly. He framed AI infrastructure as capital investment, not operating expense. It‘s not a cost center. It’s an asset that produces profit. Whether Wall Street fully buys that framing is another question. But he gave them the argument they needed to hear.

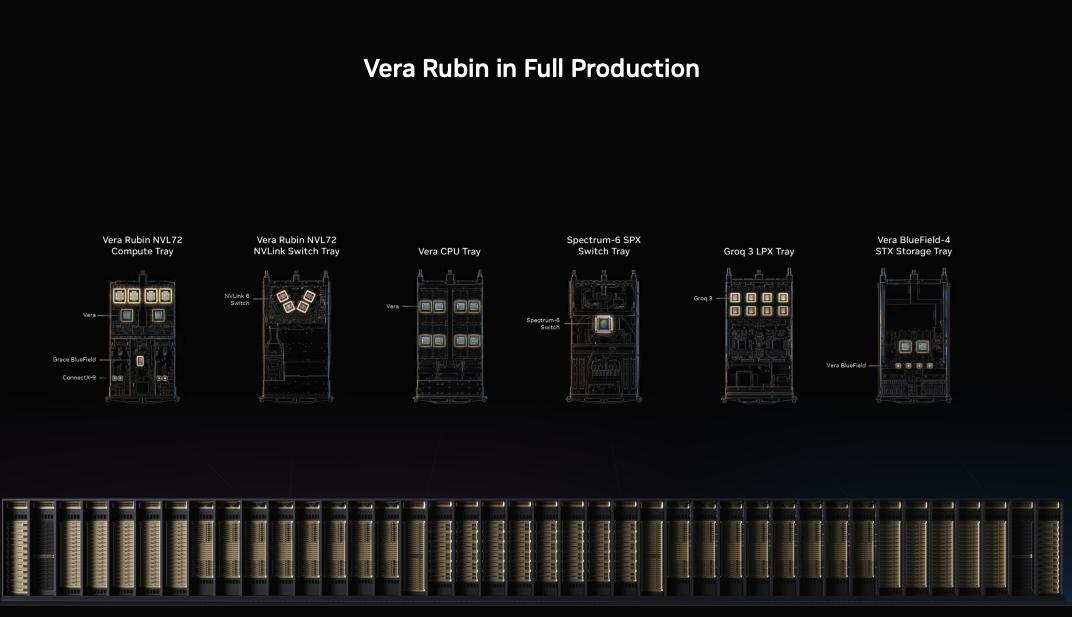

Vera Rubin Is a Bet on Agents

The hardware update matters as much as the message. Huang confirmed that Vera Rubin is now in full production. The platform is designed specifically for AI agents — not chatbots, not image generators, but systems that reason, call tools, access databases, and execute code.

The performance claims are significant. Compared to the previous Grace Blackwell generation, Vera Rubin delivers 10x higher agent throughput at scale. It‘s built to handle workloads that run for thousands of steps per prompt.

Huang positioned Vera Rubin as the answer to a specific problem. Agents need to think, retrieve, call tools, and generate responses in loops. If the CPU can’t keep up, the GPU sits idle. In an AI factory, idle GPU time is lost revenue. Vera Rubin is built to keep the entire pipeline running.

Huang also framed Vera CPU as a new growth driver. He said it could become“even more popular than GPU” because agent workloads need low-latency, high-bandwidth CPU capacity to orchestrate tool calls and memory access.

The Sell-Off Made This Speech Necessary

The shareholder meeting was about reassuring investors. The broader AI sell-off earlier this week, triggered by SK Hynix‘s rumored production shift, showed how fragile sentiment has become.

Huang’s message worked like a counterweight. Nvidia‘s revenue grew 65% to $216 billion last year. Data center revenue alone hit $194 billion, up 68%. The numbers back up the narrative. The company also committed to returning 50% or more of free cash flow to shareholders through buybacks and dividends.

He also pointed to sovereign AI as a major demand driver. Countries are building their own AI infrastructure, and Nvidia is positioned as the supplier of first resort.

The Real Question Is Not Whether Nvidia Can Ship

Huang‘s shareholder meeting was a defense of the AI investment thesis. He gave investors the argument they needed to stay in the trade. Vera Rubin’s full production status confirms that Nvidia‘s product roadmap is on track. And the broader framing — tokens as profit, data centers as factories, agents as the next wave — is designed to keep the valuation story intact.

The real question isn’t whether Nvidia can ship chips. It‘s whether customers can actually generate enough token revenue to justify the infrastructure spend. Huang says they can. The next few quarters of earnings reports from cloud providers and AI labs will tell the real story.

P.S. Huang says data centers are“factories that manufacture tokens.” At $3.4 trillion market cap, that makes Nvidia the most expensive factory equipment supplier in history. The good news: factories don’t unionize. Yet.